Should You Sell or Hold Your House in 2026? A 5-Year Wealth Comparison

A homeowner framework for comparing selling now against holding, renting, or waiting.

Selling a home is not just a price decision. It is a wealth decision, a cash-flow decision, a tax-risk decision, and a life-timing decision. In 2026, many homeowners have equity but also face higher replacement costs, higher mortgage rates than their old loans, rising insurance costs, and uncertainty about where prices go next.

The right question is not “Can I sell for a profit?” The better question is “Will I be better off selling now or holding for my real timeline?”

Quick answer

You should consider selling if your net sale proceeds, after moving and investing or using the money elsewhere, create a better five-year outcome than holding the home. You should consider holding if future equity growth, principal paydown, rental potential, or lifestyle value outweigh ongoing ownership costs and resale risk.

The clean comparison is: sell-now wealth versus hold wealth. Do not treat mortgage principal as a cost. Principal paydown increases equity. Interest, taxes, insurance, HOA dues, maintenance, and repairs are true ownership costs.

The two paths homeowners should compare

Path 1: Sell now

The sell-now path starts with your expected sale price and subtracts costs.

Net sale proceeds = sale price - mortgage payoff - agent commissions - closing costs - repairs/credits - taxes if applicable - moving costs.

Then decide what happens to the proceeds. You may invest them, use them for a new down payment, pay off debt, build cash reserves, or fund a move.

If you sell and rent, your five-year sell path might look like this:

Net sale proceeds invested - rent paid + investment growth.

Path 2: Hold

The hold path starts with future home value and subtracts future obligations.

Hold wealth = future home value - future mortgage balance - future selling costs.

Then account for the cash cost of keeping the home: mortgage interest, property taxes, insurance, HOA, maintenance, repairs, and any negative rental cash flow if you move and rent it out.

Why principal should not be counted as a cost

Many homeowners make the sell-vs-hold decision harder by treating the whole mortgage payment as an expense. That is not accurate.

The mortgage payment has two parts:

- Principal: reduces your loan balance and builds equity.

- Interest: true cost paid to the lender.

Property taxes, insurance, HOA dues, maintenance, and repairs are also true costs. Principal is cash flow, but it is not lost in the same way. A strong sell-vs-hold model separates cash flow from wealth.

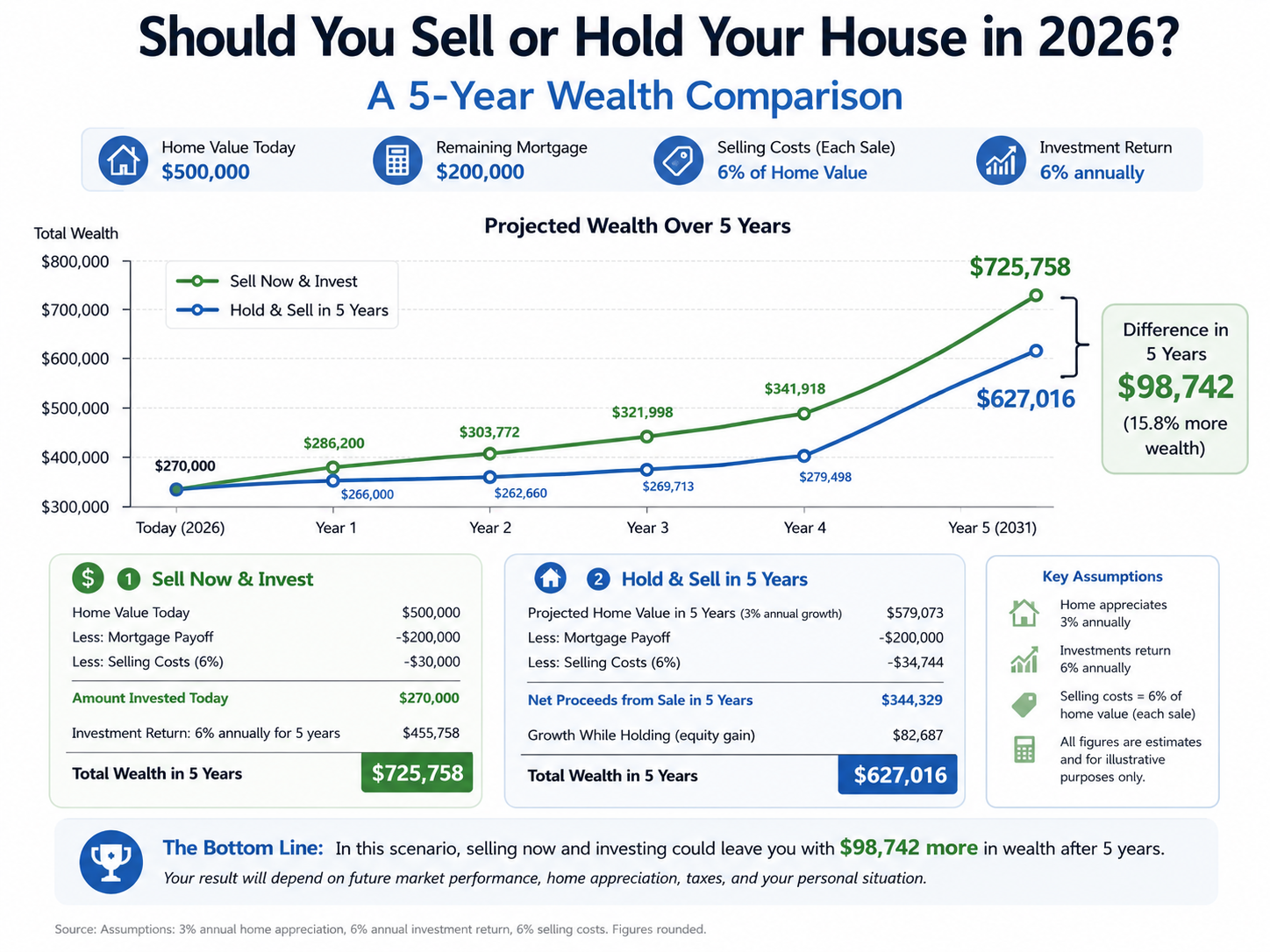

Example: sell now or hold five more years

Assume a homeowner has a home worth $800,000 and a mortgage balance of $480,000. They are deciding whether to sell now or hold for five years.

| Input | Sell now | Hold five years |

|---|---|---|

| Current home value | $800,000 | $800,000 |

| Mortgage balance | $480,000 | $480,000 today |

| Selling cost | 6% | 6% in year five |

| Net sale proceeds today | about $272,000 | N/A |

| Appreciation assumption | N/A | 3% per year |

| Future home value | N/A | about $927,000 |

| Future mortgage balance | N/A | depends on amortization |

| Future selling cost | N/A | about $55,600 |

If the homeowner sells now and invests $272,000 for five years, the sell path depends on investment return and rent or replacement housing costs. If the homeowner holds, the outcome depends on appreciation, principal paydown, future selling costs, and ownership costs.

A homeowner with a low mortgage rate, stable job, and strong neighborhood demand may benefit from holding. A homeowner with major repairs coming, a need to relocate, or a better use for the equity may benefit from selling.

The five-year wealth comparison

To compare the paths, estimate each year:

1. Home value. 2. Remaining loan balance. 3. Selling costs. 4. Non-principal ownership costs. 5. Net rent if the home becomes a rental. 6. Investment growth if proceeds are sold and invested. 7. Replacement housing cost if you sell and rent.

At year five, compare:

Sell path: invested proceeds minus rent paid or replacement housing costs.

Hold path: future home equity minus future selling costs, adjusted for cash costs or rental income.

When selling now can make sense

You need the equity for a better use

Equity is valuable, but it is not liquid unless you sell, refinance, or borrow. If selling lets you reduce risk, move closer to work, buy a more suitable home, or strengthen your cash position, the decision may be about more than appreciation.

Your home has major upcoming repairs

A roof, HVAC system, foundation issue, plumbing problem, or insurance risk can change the economics of holding.

Your location no longer fits your life

A home can be a good asset and still be the wrong home. Commute, schools, family needs, stairs, yard work, and neighborhood fit matter.

Your market has weak resale demand

If local demand is soft, holding exposes you to price and liquidity risk. A static home value estimate may not show that risk.

When holding can make sense

You have a low mortgage rate

A low-rate mortgage can be a valuable asset. Selling may force you into a higher-rate purchase or more expensive rent.

You have positive rental potential

If the home can rent for enough to cover true costs and risk, holding may create optionality.

You expect to return

If a move is temporary, selling and later rebuying may create unnecessary transaction costs.

The home has strong long-term demand

Homes with durable location advantages, flexible layouts, and manageable operating costs can be easier to hold.

How taxes fit into the decision

Taxes can change the answer. Primary residence exclusion rules, capital gains exposure, depreciation recapture for rentals, state taxes, and timing all matter. Do not rely on a generic tax assumption for a large decision.

A practical calculator can use a default assumption, but homeowners should verify with a tax professional before selling, especially if the home was rented, partially used for business, inherited, or has a large gain.

The rent-out alternative

Some homeowners do not need to choose only sell or hold as a primary residence. They can move and rent out the existing home.

Evaluate:

- Market rent.

- Vacancy.

- Property management.

- Repairs.

- Insurance changes.

- HOA rental restrictions.

- Local landlord rules.

- Debt service.

- Tax reporting.

- Your willingness to manage risk.

A home that has positive cash flow after all costs may be worth holding. A home that loses cash every month can still be worth holding if appreciation is strong, but that is a more speculative decision.

How HomeDecisionLab helps

Use the Sell vs Hold calculator at Sell vs Hold calculator to compare the wealth path of selling now against holding. The analysis should separate principal paydown from true costs and compare the future value of each path.

If you are also considering refinancing before deciding, use Refinance calculator to see whether the refinance improves the hold path or only lowers the short-term payment.

FAQ

Should I sell my house in 2026?

You should consider selling if the net sale proceeds and your next housing plan create a better financial and lifestyle outcome than holding. The answer depends on equity, mortgage balance, market demand, repairs, taxes, and what you would do after selling.

How do I compare selling vs holding?

Compare sell-now wealth against hold wealth over the same time period. Include net sale proceeds, investment returns, rent or replacement housing, future home value, future mortgage balance, selling costs, and true ownership costs.

Is mortgage principal a cost when deciding to hold?

Principal is a cash payment but not a true cost because it reduces your loan balance. Interest, taxes, insurance, HOA dues, maintenance, and repairs are true costs.

Should I rent out my house instead of selling?

Renting out the home may make sense if rent covers the true costs, the property is manageable, local rules allow it, and you are comfortable with landlord risk. It is not automatic passive income.

How do repairs affect selling vs holding?

Repairs matter in both paths. Selling may require credits or pre-listing work. Holding may require future capital spending. Large repairs can reduce the benefit of waiting.

What if I have a very low mortgage rate?

A low rate can make holding more attractive because your financing cost may be difficult to replace. But low rates do not erase taxes, insurance, maintenance, repairs, or lifestyle needs.

Data sources and assumptions used in this article

This article is educational and uses public market context plus example calculations. Numbers should be refreshed before publishing if HomeDecisionLab has newer internal data.

- Freddie Mac Primary Mortgage Market Survey context: 30-year fixed-rate mortgage averaged 6.52% for the week reported June 11, 2026.

- FHFA House Price Index context: U.S. home prices were up 1.7% year over year in Q1 2026 and up 0.5% from Q4 2025.

- U.S. Census/ACS housing-cost framing: ownership cost includes more than the mortgage payment, including taxes, insurance, utilities, fees, and other required housing expenses.

- RentCast can be used for static data snapshots where available: rent estimates, value estimates, comps, property records, listings, and local market trend data. Do not expose an API key in public blog code.

Source URLs:

- https://www.globenewswire.com/news-release/2026/06/11/3310694/0/en/Mortgage-Rates-Average-6-52.html

- https://www.fhfa.gov/reports/house-price-index/2026/Q1

- https://www.census.gov/acs/www/about/why-we-ask-each-question/housing/

- https://www.census.gov/newsroom/press-releases/2025/acs-5-year-estimates.html

- https://developers.rentcast.io/reference/rent-estimate-long-term

- https://www.rentcast.io/api

Educational disclaimer

HomeDecisionLab is an educational decision-support tool, not a lender, real estate broker, tax advisor, or financial advisor. This article should not be treated as personal financial, legal, lending, investment, or tax advice. Buyers and homeowners should confirm numbers with qualified professionals before making an offer, refinancing, selling, renting, or moving.

Educational only. This is not financial, legal, tax, mortgage, investment, or real estate advice.