Should You Refinance Your Mortgage in 2026? Break-Even, Term Reset, and Cash-Out Guide

A refinance decision guide that goes beyond monthly savings and checks break-even, term reset, closing costs, and cash-out risk.

A refinance can lower your payment and still be a bad deal. It can increase your payment and still be a smart deal. The difference depends on why you are refinancing, how long you plan to keep the loan, how much the refinance costs, and whether you are resetting the clock on your mortgage.

In 2026, homeowners should be especially careful because many existing loans were originated at lower rates. A refinance should be measured against your current loan, your planned stay, and your total home cost, not against a generic promise of “monthly savings.”

Quick answer

You should refinance if the benefit of the new loan is greater than the closing costs, term reset, and added risk. The most common reasons are lowering the rate, reducing monthly payment, shortening the term, removing PMI, switching loan type, or using cash-out proceeds strategically. But the refinance should pass a break-even test and a lifetime-cost test before you move forward.

Lower payment does not automatically mean better refinance. Sometimes it only means you stretched the debt over more years.

The refinance formula that matters

Start with three questions:

1. How much does the refinance cost? 2. How much does it improve your monthly or long-term position? 3. How long will you keep the new loan?

The basic break-even formula is:

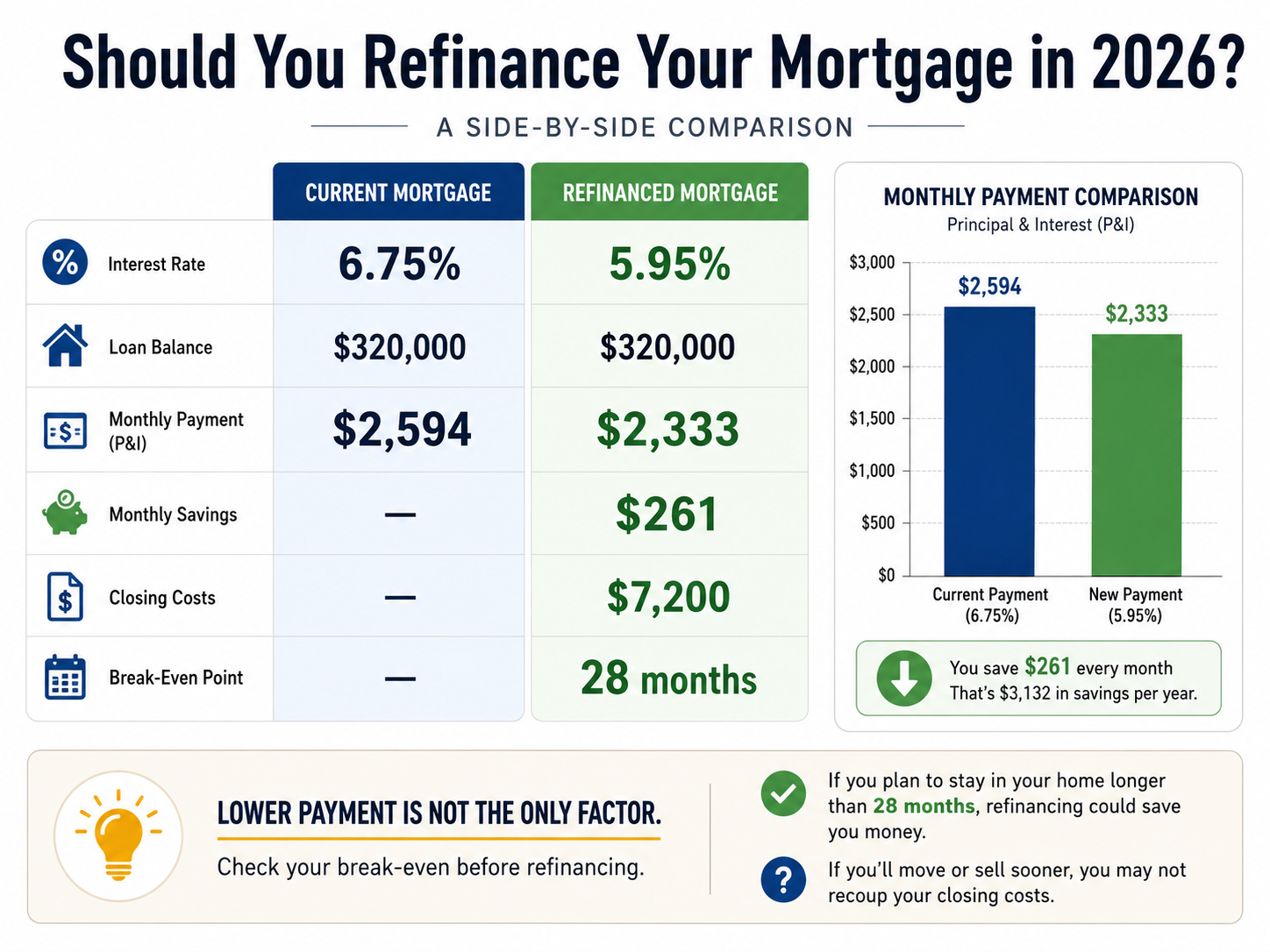

Break-even months = refinance closing costs / monthly savings.

If closing costs are $6,000 and the refinance saves $250 per month, the simple break-even is 24 months.

But simple break-even is not enough. You also need to check:

- Remaining interest on your current loan.

- Total interest on the new loan.

- Whether costs are paid in cash or rolled into the new loan.

- Whether the new loan extends the payoff date.

- Whether cash-out proceeds are used productively or consumed.

- Whether you plan to sell before the break-even point.

The four refinance tests

1. Payment test

Does the new loan improve monthly cash flow enough to matter? A small savings may not justify costs unless you will keep the loan for a long time.

2. Break-even test

Will you keep the home and loan long enough to recover closing costs? If you sell or refinance again before break-even, the refinance may be a loss.

3. Lifetime-cost test

Does the refinance reduce total interest and total home cost over your actual timeline? This is where many payment-focused refinances fail.

4. Risk test

Does the refinance increase risk by raising the loan balance, removing equity, changing loan type, or extending debt into retirement or a future move?

Example: lower payment but higher long-term cost

Assume a homeowner has 24 years left on a current mortgage. The current payment is $2,900 per month. A new 30-year refinance lowers the payment to $2,650 per month, saving $250 per month. Closing costs are $7,500 and are rolled into the new loan.

| Item | Current loan | New refinance |

|---|---|---|

| Remaining term | 24 years | 30 years |

| Monthly payment | $2,900 | $2,650 |

| Monthly savings | N/A | $250 |

| Closing costs | N/A | $7,500 |

| Simple break-even | N/A | 30 months |

| Payoff date | sooner | later |

The refinance may help cash flow, but it extends the loan by six years. If the homeowner only looks at monthly savings, it looks great. If they look at total interest and payoff date, the answer may be different.

When refinancing can be smart

You can lower the rate enough and stay past break-even

Rate improvement is one of the clearest reasons to refinance, but it still needs a cost test.

You can remove PMI

Removing PMI may create meaningful savings without the same tradeoffs as a larger cash-out loan.

You can shorten the term without straining cash flow

Moving from a 30-year to a 15-year or 20-year loan can reduce interest, but only if the higher payment is sustainable.

You need to change loan type

Switching from an adjustable-rate mortgage to a fixed-rate mortgage may reduce future payment risk.

You use cash-out proceeds for a high-value purpose

Cash-out may make sense for necessary repairs, debt restructuring, or investment in the property. It is riskier when used for short-lived spending.

When refinancing can be a trap

You restart the 30-year clock without noticing

A lower payment can hide the fact that you are paying for longer.

You roll costs into the loan and ignore them

Rolled-in costs still count. They increase the loan balance and can increase long-term interest.

You refinance before selling soon

If you expect to sell in one or two years, the refinance may not reach break-even.

You use cash-out to fund spending that does not build value

Cash-out converts home equity into debt. That can be useful, but it should be deliberate.

You compare only rate, not total cost

The lowest advertised rate is not automatically the best loan. Points, fees, term, and closing costs matter.

How to evaluate a cash-out refinance

For cash-out, ask:

- How much equity remains after the refinance?

- What is the new loan-to-value ratio?

- What is the new monthly payment?

- How will the cash be used?

- Does the use of cash increase net worth or reduce risk?

- What happens if home values decline?

- Would a HELOC, home equity loan, or no loan be better?

Cash-out is not free money. It is a new debt secured by your home.

How HomeDecisionLab helps

Use the refinance calculator at Refinance calculator. A useful refinance analysis should show current loan cost, new loan cost, full timeline comparison, planned-stay comparison, break-even timing, cash-out received, and whether closing costs are paid in cash or rolled into the loan.

If you are refinancing because you are unsure whether to sell or hold, run Sell vs Hold calculator too. Sometimes the better decision is not a refinance. It is selling, holding, renting out the home, or doing nothing.

FAQ

Should I refinance my mortgage in 2026?

Refinancing may make sense if the savings or strategic benefit outweighs closing costs, term reset, and added risk. It depends on your current loan, new loan, costs, and how long you plan to keep the home.

What is a good refinance break-even point?

A good break-even point is one you are very likely to exceed. If break-even is 30 months and you may sell in 18 months, the refinance is risky.

Is a lower monthly payment always better?

No. A lower payment can come from a lower rate, but it can also come from extending the loan term. Always check lifetime interest and payoff date.

Should I roll closing costs into the refinance?

Rolling costs into the loan can reduce upfront cash needs, but it increases the loan balance. It should still be counted in the analysis.

Is cash-out refinancing a bad idea?

Not always. It can be useful for strategic purposes, but it increases debt secured by your home. The use of proceeds matters.

Should I refinance if I plan to move soon?

Usually you should be cautious. If you sell before the break-even point, the refinance may not recover its costs.

Data sources and assumptions used in this article

This article is educational and uses public market context plus example calculations. Numbers should be refreshed before publishing if HomeDecisionLab has newer internal data.

- Freddie Mac Primary Mortgage Market Survey context: 30-year fixed-rate mortgage averaged 6.52% for the week reported June 11, 2026.

- FHFA House Price Index context: U.S. home prices were up 1.7% year over year in Q1 2026 and up 0.5% from Q4 2025.

- U.S. Census/ACS housing-cost framing: ownership cost includes more than the mortgage payment, including taxes, insurance, utilities, fees, and other required housing expenses.

- RentCast can be used for static data snapshots where available: rent estimates, value estimates, comps, property records, listings, and local market trend data. Do not expose an API key in public blog code.

Source URLs:

- https://www.globenewswire.com/news-release/2026/06/11/3310694/0/en/Mortgage-Rates-Average-6-52.html

- https://www.fhfa.gov/reports/house-price-index/2026/Q1

- https://www.census.gov/acs/www/about/why-we-ask-each-question/housing/

- https://www.census.gov/newsroom/press-releases/2025/acs-5-year-estimates.html

- https://developers.rentcast.io/reference/rent-estimate-long-term

- https://www.rentcast.io/api

Educational disclaimer

HomeDecisionLab is an educational decision-support tool, not a lender, real estate broker, tax advisor, or financial advisor. This article should not be treated as personal financial, legal, lending, investment, or tax advice. Buyers and homeowners should confirm numbers with qualified professionals before making an offer, refinancing, selling, renting, or moving.

Educational only. This is not financial, legal, tax, mortgage, investment, or real estate advice.